India: GST Circular for relaxing norms related to Letters of Undertaking and Bonds for Exporters

Export of Goods and Services under the GST regime have been categorized as Zero-Rated Supply. This means that subject to the provisions of the CGST Act, 2017,

Export of Goods and Services under the GST regime have been categorized as Zero-Rated Supply. This means that subject to the provisions of the CGST Act, 2017,

India: GSTR 1

The concept of GSTR 1 can be understood by the interpretation of compliances under Goods & Service Tax. Monthly return filing has been made mandatory by the recently implemented tax structure, thus making each month a taxable period for filing of a set of returns, namely GSTR 1, GSTR 2 and GSTR 3.

India: RBI issues norms on complete KYC for e-wallets

The Guidelines titled the Reserve Bank of India (Issuance and Operation of Prepaid Payment Instruments) Directions, 2017 (hereinafter referred to as the “Directions”) seek to authorize, regulate and supervise entities operating payment systems for issuance of Prepaid Payment Instruments

India: Exemption for Single Brand Retailers to state MRP on Packaged Commodities

Single brand retailers may be exempted from marking their products with Maximum Retail Price (hereinafter referred to as “MRP”), as the Government is contemplating to change labelling norms for single-brand retailers.

Single brand retailers may be exempted from marking their products with Maximum Retail Price (hereinafter referred to as “MRP”), as the Government is contemplating to change labelling norms for single-brand retailers.

India: Supreme Court of India: “No Cracker Boom”

After analyzing various factors involved in the deterioration of air quality and unhealthy effects thereto, particularly upon the advent of the winter season, the Bench of Hon’ble Justices A.K. Sikri, A.M. Sapre and Ashok Bhushan of the Supreme Court of India..

After analyzing various factors involved in the deterioration of air quality and unhealthy effects thereto, particularly upon the advent of the winter season, the Bench of Hon’ble Justices A.K. Sikri, A.M. Sapre and Ashok Bhushan of the Supreme Court of India..

India: Government constitutes National Coastal Zone Management Authority

The Ministry of Environment, Forest and Climate Change has constituted the National Coastal Zone Management Authority vide notification no. S.O. 3266(E) dated October 6, 2017

The Ministry of Environment, Forest and Climate Change has constituted the National Coastal Zone Management Authority vide notification no. S.O. 3266(E) dated October 6, 2017

India: GST Circular for relaxing norms related to Letters of Undertaking and Bonds for Exporters

Source: www.lawctopus.com

Introduction:

Exports as Zero-Rated Supplies:

Export of Goods and Services under the GST regime have been categorized as Zero-Rated Supply. This means that subject to the provisions of the CGST Act, 2017, and the Rules made thereunder, the exporter shall not be liable to pay Integrated GST applicable on exported goods if he/ she satisfies the criteria as prescribed under the Rules. The exporter can trade without payment of integrated tax followed by claim of refund of unutilized input tax credit or on payment of integrated tax with provision for refund of the tax paid.

Letter of Undertaking and Bonds:

For availing these benefits, according to Rule 96A of Central Goods and Services Tax Rules, 2017 in case of export of goods or services without payment of GST, the exporter has to furnish a bond or letter of undertaking (LUT) in form RFD-11. This is also required in the case of provision of goods or services to SEZ units/ developer.

In supersession of its July 7 Circular, the Central Board of Excise and Customs (CBEC) issued a notification – Notification No. 37/2017 – Central Tax dated October 4, 2017 extending the facility of Letters of Undertaking to all exporters under Rule 96 A of the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as “the CGST Rules”) subject to certain conditions and safeguards.

It is a significant move by the Finance Ministry to liberalize norms for letters of undertaking (LUT) to help exporters who have been facing difficulties under the Goods and Services Tax (GST) in timely shipment of consignments. The Circular also widens the scope of applicability of the said norms by relaxing the eligibility criteria of exporters who were benefited by this Zero-Rated Supply category. The facility was earlier available only for manufacturer exporters.

Significant changes made by the new Circular:

Superseding the previous circulars, CBEC’s circular issued on October 4, 2017 is commendable for 2 reasons. Firstly, because it has relaxed the eligibility norms and allowed more number of exporters to be eligible under the scheme. Secondly, it has induced ease into the compliance by making provisions for self-declarations of previous prosecutions and self- sealing of stocks and deemed acceptance of undertaking if not replied to in 3 days.

Significant aspects of the Circular:

Accordingly, to ensure uniformity the Board, in exercise of its powers conferred under Section 168 (1) of the Central Goods and Services Tax Act, 2017 clarifies the following issues:

- Eligibility to export under LUT: The eligibility criteria for being exporters to fall within the ambit of Zero Rated Supply and become entitled to the benefits of LUTs, has been relaxed considerably. Earlier, (old notification) this facility of export under LUTs was applicable only to ‘status holders’ under the Foreign Trade Policy 2015-2020 and to persons receiving a minimum foreign inward remittance of 10% of the export turnover in the preceding financial year which was not less than INR 1 Cr. The same has now been extended to all registered persons who intend to supply goods or services for export without payment of integrated tax.Exception: The only persons not entitled to this facility are those who have been prosecuted for any offence under the CGST Act or the Integrated Goods and Services Tax Act, 2017 or any of the existing laws and the amount of tax evaded in such cases exceeds INR 250 lakhs.

- Validity of LUTs and their deemed withdrawal: The LUT shall be valid for the whole financial year in which it is tendered. However, in case the goods are not exported within the time specified and the tax dues according to sub rule (1) of rule 96A of the CGST Rules are not paid the facility of export under LUT will be deemed to have been withdrawn. If the amount mentioned in the said sub-rule is paid subsequently, the facility of export under LUT shall be restored. Therefore, the Circular states that exports made during the period from when the facility to export under LUT is withdrawn till the time the same is restored.

- Steps for submission of Form for bond/LUT:

• Download FORM GST RFD-11 from www.cbec.gov.in;

• Prepare LUT on the letter head of the registered person, in duplicate, and it shall be executed by the working partner, the Managing Director or the Company Secretary or the proprietor or any other person duly authorized by them;

• Furnish a duly filled form to the jurisdictional Deputy/Assistant Commissioner having jurisdiction over their principal place of business; and

• The bond, wherever required, shall be furnished on non-judicial stamp paper of the value as applicable in the State in which the bond is being furnished.

- Self-declaration of Documents for LUT: Self-declaration to the effect that the conditions of LUT have been fulfilled shall be accepted unless there is specific information otherwise. That is, self-declaration by the exporter to the effect that

strong>he has not been prosecuted should suffice for the purposes of Notification No. 37/2017- Central Tax dated October 4, 2017. Verification, if any, may be done on post-facto basis. - Deemed Acceptance: To ensure that LUT/ Bonds are processed as a priority, as they are the sine qua none of the exports business now, the clarification states that if a duly filled and eligible LUT/ Bond is not accepted within 3 says, it shall be deemed to be accepted.

- Bank guarantee for those prosecuted under CGST laws: The circular goes a step further and grants a chance even to persons being prosecuted under CGST laws, for cases involving an amount exceeding INR 250 lakhs for them to avail the benefits of LUT/Bonds, if they can furnish a bank guarantee. A bond, in all cases, shall be accompanied by a bank guarantee of 15% of the bond amount. Export bond should be furnished on non-judicial stamp paper of the value as applicable in the State in which the bond is being furnished.

- Clarification regarding running bond: The exporters shall furnish a running bond covering the amount of self-assessed estimated tax liability on the export and ensure that the outstanding integrated tax liability on exports is well within the bond amount. Fresh bond amounts can be furnished if the estimated bond amount is exceeded and does not cover the said liability in yet to be completed exports. The exporter should maintain the debit / credit entries of integrated tax in the running bond and are to be furnished to the Central tax officer as and when required.

- Sealing by officers: Till mandatory self-sealing is operationalized, sealing of containers, wherever required to be carried out under the supervision of the central excise officer having jurisdiction over the concerned place of business. The Deputy/Assistant Commissioner having jurisdiction over the principal place of business should be sent a report of the sealing.

- Where Zero Rating in not applicable to exporters: The said zero rated taxation and LUT facility is not applicable where merchant exporters are required to purchase goods from a manufacturer or in case of supplies to export oriented units. These transactions shall be normally taxable under the GST regime.

- Realization of export proceeds in Indian Rupee: With reference to the laws relating to foreign trade and the RBI Master Circular No. 14/2015-16 dated July 01, 2015 all export proceeds shall be realized in freely convertible currency though acceptance of LUT for supplies of goods to Nepal or Bhutan or SEZ developer or SEZ unit will be permissible irrespective of whether the payments are made in Indian currency or convertible foreign exchange as long as they are in accordance with the applicable RBI guidelines. But the supply of services, however, to Nepal or Bhutan will be deemed to be export of services only if the payment for such services is received by the supplier in convertible foreign exchange.

- > Jurisdictional officer: Though the jurisdictional Deputy/Assistant Commissioner having jurisdiction over the principal place has the power to accept the LUT/ Bonds, the exporter is at liberty to furnish the LUT/bond before either the Central Tax Authority or the State Tax Authority till the administrative mechanism for assigning of taxpayers to the respective authority is implemented.

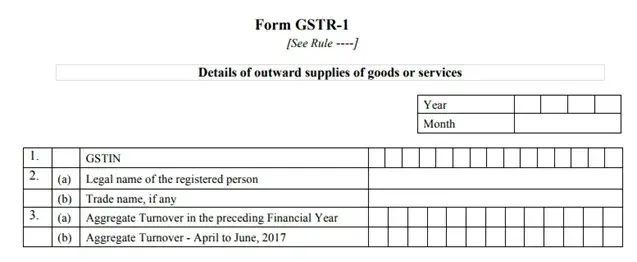

India: GSTR 1

Source : www.lawctopus.com

Introduction

The concept of GSTR 1 can be understood by the interpretation of compliances under Goods & Service Tax. Monthly return filing has been made mandatory by the recently implemented tax structure, thus making each month a taxable period for filing of a set of returns, namely GSTR 1 GSTR 2 and GSTR 3

Among these three, GSTR 1 is the detailed return prepared for the invoices raised by the sellers/ dealer towards the buyers and contains details of all the sales transactions of a registered dealer for a month. GSTR 1 forms the base document that lists the transaction of supply of goods by the business or trader.

GSTR-1 should be filed even if

there are nil returns to be filed (no business activity during a

month) in the given taxable period.

Due date for filing GSTR 1 Return

GSTR 1 return must be filed on or before the 10th of each month. In the GSTR 1 return, the taxpayer would provide details of all supplies made during the previous month. Hence, in the GSTR 1 return filed on November, details of outward supplies in the month of October would be submitted.

Who should file GSTR 1?

Every registered person is required to file GSTR 1 irrespective of whether there are any transactions during the month or not.

The following registered persons are exempted from filing the GSTR 1:

- Suppliers of online information and database access or retrieval services (OIDAR), who have to pay tax themselves (as per Section 14 of the IGST Act) • Input Service Distributor (they have to file GSTR 6)

- Non-Resident Taxable person (they have to file GSTR 5)

- Composition Scheme Taxpayer under section 10. (they have to file GSTR 4)

- Tax Deductor at source under Section 51 (they have to file GSTR 7)

- Tax collector at Source under Section 52 (they have to file GSTR 8)

What is the penalty for not filing GSTR 1 Return?

A default notice under section 46 of the CGST Act will be served, in case any fails to file the return and will be liable to pay the tax amount along with interest on the outstanding amount. Per day penalty of Rs.100 will be applicable for each day of default up to a maximum amount of Rs.5000.

Effects on other Filings

GSTR 1 is the base document on the basis of which the rest of the returns are auto-populated. As the supplier of goods or services enters details of invoices raised by him towards the buyer of goods or services, an intimation of the same is sent to the buyer confirming the same in the form of GSTR 2A. Once the said transaction is confirmed at the buyer’s end, the details of which get auto-populated in the GSTR 2 at the suppliers end.

Or else, in case of discrepancy, this detail gets filed under GSTR 1A at the supplier’s end for further modification or rectification.

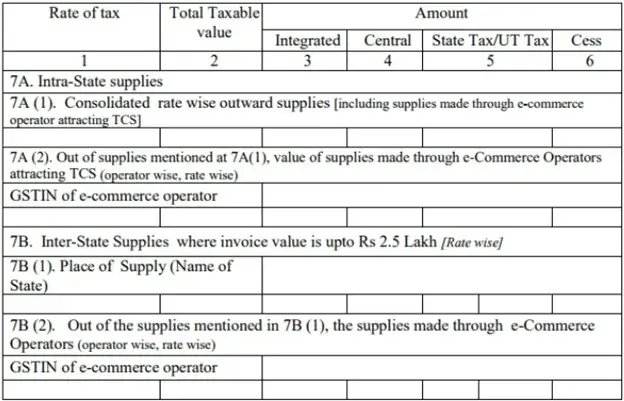

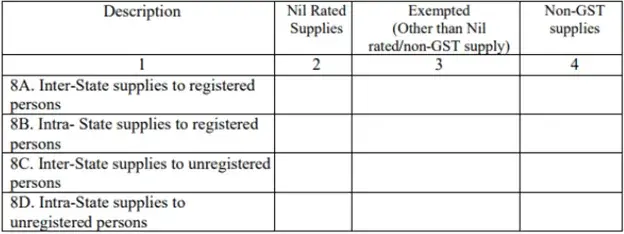

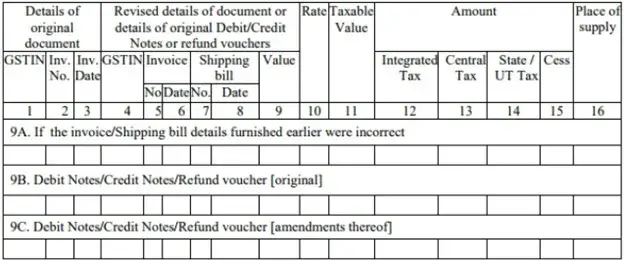

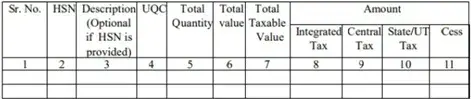

Particulars to be filed under GSTR 1

- GSTIN/Legal Name of the Entity/Aggregate Turnover for Previous Financial Year

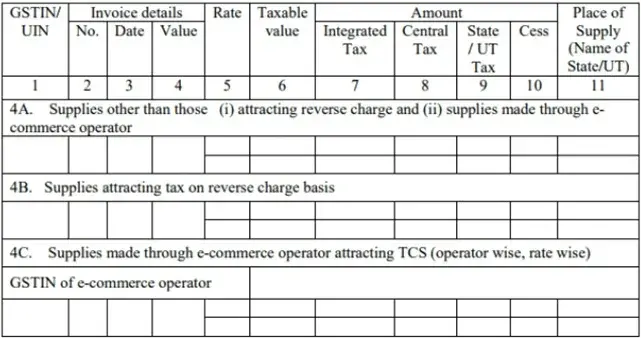

- Taxable Outward Supplies to Registered Persons

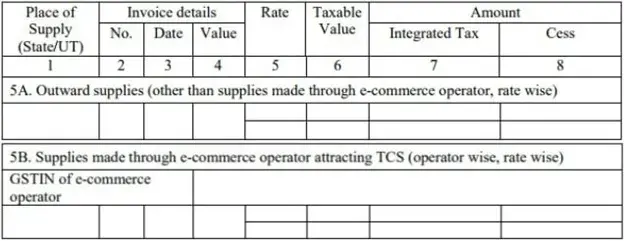

- Taxable outward inter-State supplies to unregistered persons where the invoice value is more than Rs 2.5 lakh

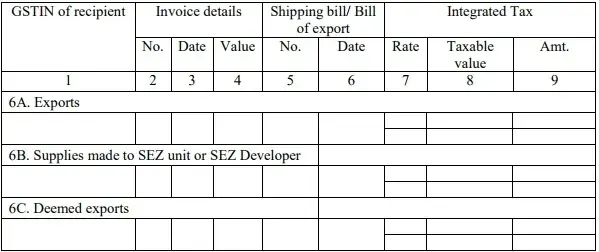

- Zero-rated supplies and deemed exports

- Taxable Supplies Made to Unregistered Persons

- Nil-rated, exempt and non-GST outward supplies

- Amendments to Taxable Supplies

- Amendments to taxable outward supplies to unregistered persons furnished on returns for earlier tax periods

- Consolidated Statement of Advances Received or adjusted in the current tax period

- HSN-wise summary of outward supplies

- Documents issued during the tax period

India: RBI issues norms on complete KYC for e-wallets

Source : www.rbi.org.in

Introduction

The Reserve Bank of India (hereinafter referred to as “RBI”) has prepared new norms for protection of wallet users from fraudulent transactions, vide Circular RBI/DPSS/2017-18/58 dated October, 11, 2017.[1]

The Guidelines titled the Reserve Bank of India (Issuance and Operation of Prepaid Payment Instruments) Directions, 2017 (hereinafter referred to as the “Directions”) seek to authorize, regulate and supervise entities operating payment systems for issuance of Prepaid Payment Instruments (hereinafter referred to as “PPIs”) in the country. PPIs are payment instruments that facilitate purchase of goods and services, including financial services, remittance facilities, etc. against the value stored on such instruments.[2] PPIs can be issued as smart cards, magnetic stripe cards, internet accounts, online wallets, mobile accounts, mobile wallets, paper vouchers and any such instruments used to access the prepaid amount.

Conversion to KYC compliant PPI

According the Directions, Bank and non-bank issuers of PPIs are permitted to issue PPIs after obtaining minimum details of the PPI holder which includes mobile number verified with One Time Pin (OTP) and self-declaration of name and unique identification number of official documents. However, the PPIs will be converted into KYC (Know Your Customer) compliant semi-closed PPIs within a period of 12 months from the date of issue of PPI, on the failure of which no further credit shall be allowed in such PPIs. All existing wallet users have to convert to the full KYC format by the end of this calendar year.

Features of PPIs

These PPIs shall be reloadable in nature and issued only in electronic form, including cards. The maximum amount that can be loaded in PPIs cannot exceed INR 10,000 in any month and cannot exceed INR 1,00,000 in any financial year. Also, the total amount debited from such PPIs shall not exceed INR 10,000 in any given month.

The PPIs can be used only for purchase of goods and services. No funds may be transferred from such PPIs to bank accounts and also to PPIs of same / other issuers. Further, there is no separate limit on purchase of goods and services using PPIs and PPI issuer may decide limit for these purposes within the overall PPI limit.

Issuance of PPIs

Banks and non-bank entities have been issuing PPIs in India after obtaining necessary approval / authorization from RBI under the Payment and Settlement Systems Act, 2007 (hereinafter referred to as “PSS Act”). The Directions state that all non-bank entities seeking authorization from RBI under the PSS Act shall have a minimum positive net-worth of INR 5 crore as per the latest audited balance sheet at the time of submitting application for approval. Thereafter, by the end of the third financial year from the date of receiving final authorization from RBI, the entity shall have a minimum positive net-worth of INR 15 crore which shall be maintained at all times. RBI has thus strengthened norms relating to PPIs by introducing provision of fulfilling completing KYC requirements, although entities have been given time to convince customers to complete KYC requirements. Also, PPIs are now comprehended to be serious financial services as RBI has increased the eligibility criteria of entities seeking approval for authorization of PPIs.

———————————–

[1]Available at https://rbidocs.rbi.org.in/rdocs/notification/PDFs/58PPIS11102017

A79E58CAEA28472A94596CFA79A1FA3F.PDF

[2]Section 2.3 of the Directions

India: Exemption for Single Brand Retailers to state MRP on Packaged Commodities

Source : Consumeraffairs.nic.in

Introduction:

Single brand retailers may be exempted from marking their products with Maximum Retail Price (hereinafter referred to as “MRP”), as the Government is contemplating to change labelling norms for single-brand retailers. This is in furtherance to discussions of the European Business Group (hereinafter referred to as “EBG”) with the Government to change labelling norms for single-brand retailers. EBG, a federation in India which aims to create an environment for European Business to flourish, is currently in talks with the Government to amend the current labelling norms in India with respect to writing of MRP, date of manufacture and other details on packaged commodities for sale in the Indian market.

Law on MRP in India:

All packaged goods in India have to mandatorily bear MRP. MRP is the maximum price at which a commodity in packaged form may be sold to the consumer inclusive of all taxes. MRP was introduced in 1990 vide amendment to the Standards of Weights and Measures Act (Packaged Commodities’ Rules), 1997. Prior to this amendment, manufacturers had the option to print either the MRP (inclusive of all prices) or the retail price (local taxes extra). However, manufacturers often charged more that the locally applicable taxes by opting for the later method. Therefore, the amendment was introduced to prevent consumers from profiteering by manufacturers and to introduce compulsory printing of MRP on all packaged commodities.

Currently, provisions of MRP and manner of declaration of MRP are governed by The Legal Metrology (Packaged Commodities) Rules,[1] 2011 (hereinafter referred to as the “Rules”). According to the Rules, all packaged commodities shall be affixed with a label that is legible and prominent, and such label shall contain declarations including the MRP.[2] The Rules make no labelling exceptions for single brand retailers or any kind of manufactures, and state that all packaged commodities have to bear MRP. Therefore, doing away with the provision for MRP will require legislative changes and amendments in the law.

Impact of stating MRP:

The law of MRP in India is unique as India is one of the few countries where there is mandatory provision of displaying MRP on products. In most countries, displaying the MRP tag is not mandatory and the price is generally labelled on the shelf where a bunch of products are displayed. The provision of MRP was introduced in India to protect the interest and right of consumers. Affixing labels on packages with details including MRP allows consumers to make an informed decision and obtain full information about the quality and price of products they purchase.

However, according to European retailers, the practice of affixing labels on packaged commodities increases cost of production for single brand retailer. According to them, as there are no middlemen involved between manufacturers and consumers in case of single brand retailers, therefore, MRP is not needed to protect consumer rights.[3] Also, if no MRP is to be printed on affixed labels, the cost of production will decrease which will ultimately lead to reduction in price of commodities for consumers.

The Government, now, has to decide and strike a balance between protecting the rights of consumers and ensuring more investments and ease of doing business for European retailers. Also, it is hoped that new rules are framed in a manner which will allow standard pricing of goods sold over the counter in local stores, and there is no scope for arbitrary pricing.

———————————–

[1] “Single brand retailers may not need to quote MRP” by John Sarkar and Dipak K Dash, published in the Times of India on October 7, 2015 available at https://timesofindia.indiatimes.com/business/india-business/single-brand-retailers-may-not-need-to-quote-mrp/articleshow/60978891.cms

[2] Section 6 of the Rules

[3] “Single brand retailers may not need to quote MRP” by John Sarkar and Dipak K Dash, published in the Times of India on October 7, 2015 available athttps://timesofindia.indiatimes.com/business/india-business/single-brand-retailers-may-not-need-to-quote-mrp/articleshow/60978891.cms

India: Supreme Court of India: “No Cracker Boom”

Source : supremecourtofindia.nic.in

Introduction

After analyzing various factors involved in the deterioration of air quality and unhealthy effects thereto, particularly upon the advent of the winter season, the Bench of Hon’ble Justices A.K. Sikri, A.M. Sapre and Ashok Bhushan of the Supreme Court of India in the case of

Arjun Gopal & Others Vs Union of India & Others (IA NO. 92862 OF 2017

in Writ Petition (Civil) No. 728 OF 2015) dated October 9, 2017 imposed suspension on the sale of the firecrackers till November 1, 2017.

Brief Facts

The present judgement arose consequential to the petitions filed against the orders of the Supreme Court dated September 12, 2017, modifying the sale of fire-crackers. The order of the Court dated September 12, 2017, lifted the suspension on permanent licenses, thereby, permitting them to exhaust their stock of fireworks in Delhi-NCR and putting such licencees to notice for Dussehra and Diwali in 2018 restricting them to possess and sell only 50% of the quantity permitted in 2017 and that this will substantially reduce over next couple of years. The Court while assessing the dire need of improving the air quality, considered it appropriate to adopt a graded and balanced approach, which is necessary and would reduce and gradually eliminate air pollution caused due to cracker bursting.

Decision

The Hon’ble Supreme Court while reiterating the November 2016 decision suspended the temporary licenses that was issued by the police after the passing of the order dated September 12, 2017, in order to prevent further sale of the crackers in Delhi and NCR. However, the Court stopped short of a complete ban, and allowed permanent license holders to either exhaust their existing stock of fireworks, or take measures to transport the stocks outside of Delhi and NCR.

Rationale

The Court made the following observations while arriving at its decision:

- Taking into account the poor environmental conditions witnessed last year where pollution levels rose at an alarming level making Delhi the most polluted city in the world, the Court held that though, the bursting of firecrackers was not the sole cause resulting in such high degree of pollution, but it was a major contributing element for the same.

- The Court acknowledged the efforts made by Government (Ministry of Environment, Government of India as well as Delhi Government), Media, NGOs and various other groups to create awareness amongst the general public about the ill-effects of bursting of these crackers.

- The Court recognized the stand taken by CPCB (Central Pollution Control Board) that Sulphur in fireworks should not be permitted as Sulphur on combustion produces Sulphur Dioxide and the same is extremely harmful to health. The CPCB also stated that between 9:00 pm to midnight on Diwali day the levels of Sulphur Dioxide content in the air is dangerously high.

- The Court concluded that the order suspending the licences should be given one chance to test itself in order to find out as to whether there would be positive effect of this suspension, particularly during the Diwali period. In considering the adverse effects of burning of crackers leading to the depreciation of the air quality deteriorates abysmally and gives rise to severe “health emergency” situations every year post Diwali in the year 2016, the Court had passed the order dated November 11, 2016 but it’s the impact remains to be tested during Diwali days.

- The Court held that the directions issued under the order dated September 12, 2017 passed by the Court should be made effective only from November 01, 2017 i.e. post Diwali, thus delaying its enforcement.

Response by the Society

The aforesaid decision received warm welcome from various strata of the society. Many doctors have appreciated the decision and explained the damaging impact of the increased pollution levels caused due to the bursting of crackers. The accelerated quantity of particulate matter in the air causes various problems like breathlessness, coughing fit, chest tightness, asthma, pulmonary disease, rhinitis and pneumonia.

Environmentalists, elderly citizens and students have also shown enthusiasm towards the decision considering it beneficial in the longer run. Even religious institutions have supported the decision and promoted the spread of the thought of not bursting crackers on the pretext of linking them with the traditions of the festivals.

Conclusion

Although the Supreme Court has come forward with a pragmatic approach with the intention to control and reduce the pollution caused by restricting the bursting of crackers of festivals like Diwali, the move remains incomplete as the aforesaid order merely prevents the sale of crackers and does not bring within the ambit of its decision, the prohibition on their bursting which causes pollution. The Court explained the hardships which may be encountered to monitor and prevent the burning of crackers by the people.

More stringent actions should be taken to prevent causing of pollution by burning of crackers which not only contaminates the environment making it unfit for all forms of life but also creates noise which may increase palpitations among humans as well as animals. The Environmental law regime enshrines the polluter pays principle which imposes liability on the person polluting the environment to compensate for the damage caused and thus return the environment to its original state. Strict measures should be imposed upon those who cause pollution including those burning crackers.

Other allied problems associated with the burning of crackers include the generation of a lot of trash and the shops selling them remain vulnerable to fire which results in major injuries, loss of life and damage to property.

Despite numerous efforts being made by the Government, Media, NGOs and like campaigns, it remains the indispensable responsibility of the individuals to understand the detrimental effect being caused on the environment by cracker burning. It is essential not only to comply with the fundamental duty as prescribed by the Constitution under Article 51-A (g) to have compassion to their surrounding environment but also to respect the moral duty that vests towards the protection of the mother nature thereby making it a better place to live.

Lastly, as reported by

Hindustan Times[1], after the ban, New Delhi witnessed its cleanest Diwali in three years, even though pollution still soared. Last year, Diwali had triggered the worst smog in 17 years, forcing the Delhi government to shut down schools and construction sites. It was Delhi’s worst Diwali in terms of air quality as a deadly cocktail of harmful pollutants and gases engulfed the city in thick smog.

According to data and monitoring by the System of Air Quality and Weather Forecasting and Research, commonly known as SAFAR, and the Central Pollution Control Board, Delhi, on Thursday had an air quality index (AQI) of 319, which falls in the very poor category. However, this was much better than 2016 when AQI on Diwali was 431 and 343 in 2015.

———————————

India: Government constitutes National Coastal Zone Management Authority

Source : Envfor.nic.in

Introduction

The Ministry of Environment, Forest and Climate Change has constituted the National Coastal Zone Management Authority vide notification no. S.O. 3266(E) dated October 6, 2017 (hereinafter referred to as the “Authority”).

The Central Government constituted the Authority, in exercise of the powers conferred under sub-sections (1) and (3) of section 3 of the Environment (Protection) Act, 1986 (hereinafter referred to as “EPA”).

- Section 3(1) – It grants the Central Government with the power to take all such measures as it deems necessary for the purpose of protecting and improving the quality of the environment and preventing, controlling and abating environmental pollution.

- Section 3(3) – If it is considered necessary by the Central Government to do for the purposes of the EPA, then it may constitute an authority for the purpose of exercising and performing such of the powers and functions of the Central Government under EPA.

Environment (Protection) Act, 1986

Enacted in 1986, it is one of the most comprehensive legislations with an intent to protect and improve the environment. Article 48A under the Constitution of India specifies that the State shall endeavor to protect and improve the environment and to safeguard the forests and wildlife of the country. The objectives of this Act are as follows:-

- To protect and improve the environment qualities

- To cover all the problems of environment

- To create an authority with the purpose of environmental protection

- To provide a deterrent punishment to those who endanger human environment, safety and health

National Coastal Zone Management Authority

The Authority constituted by the Central Government has its principal focus on the coastal environment. The main purpose for constitution of the Authority is protection and improving the quality of the coastal environment and preventing, abating and controlling environmental pollution in the coastal areas.

The Authority shall have its headquarters at New Delhi. The list of persons appointed at various designations under the Authority can be found in the Official Gazette of India.[1] The minimum number of members required to initiate a valid meeting of the Authority shall be ten (10). The powers and functions of the Authority are as follows:-

- To co-ordinate the actions of the State Coastal Zone Management Authorities (SCZMA) and the Union Territory Coastal Zone Management Authorities (UTZMA) under the EPA and the Rules made thereunder, or under any other law which is relatable to the objects of the said EPA

- To review cases involving violations of the provisions of the EPA and the Rules made thereunder, either suo-motu, or on the basis of complaint made by an individual or body, or organization, and issue directions wherever necessary, under section 5 (Power to give directions) of the EPA.

- To make specific recommendations to the Central Government after examining the proposals for changes or modifications in the clarification of Coastal Zone Areas and in the Coastal Zone Management Plans received from the SCZMA and the UTZMA.

- File complaints under section 19 (Cognizance of Offence) of the EPA in cases of non-compliance of the directions issued by it.

- To inspect the facts concerning the cases before it.

- To provide technical assistance and guidance to various Government Authorities and other institutions or organizations as may be found necessary, in the matters relating to protection and improvement of coastal environment.

- To advise the Central government on policy, planning, research and development, setting up of centres of excellence and funding, in matters relating to Coastal Regulation Zone Management.

- To deal with all environmental issues relating to coastal regulation zone which may be referred to it by the Central Government.

- To place information regarding the agenda and minutes of its meetings in the public domain, including through internet website www.envfor.nic.in.

- Whenever required, to invite any other expert as a member during its meeting.

- The foregoing powers and functions of the Authorities shall be subject to the supervision and control of the Central Government.

—————————