Source :www.lawctopus.com

Introduction

The concept of GSTR 1 can be understood by the interpretation of compliances under Goods & Service Tax. Monthly return filing has been made mandatory by the recently implemented tax structure, thus making each month a taxable period for filing of a set of returns, namelyGSTR 1,GSTR 2 andGSTR 3.

Among these three, GSTR 1 is the detailed return prepared for the invoices raised by the sellers/ dealer towards the buyers and contains details of all the sales transactions of a registered dealer for a month. GSTR 1 forms the base document that lists the transaction of supply of goods by the business or trader.

GSTR-1 should be filed even if there are nil returns to be filed (no business activity during a month) in the given taxable period.

Due date for filing GSTR 1 Return

GSTR 1 return must be filed on or before the 10th of each month. In the GSTR 1 return, the taxpayer would provide details of all supplies made during the previous month. Hence, in the GSTR 1 return filed on November, details of outward supplies in the month of October would be submitted.

Who should file GSTR 1?

Every registered person is required to file GSTR 1 irrespective of whether there are any transactions during the month or not.

The following registered persons are exempted from filing the GSTR 1:

- Suppliers of online information and database access or retrieval services (OIDAR), who have to pay tax themselves (as per Section 14 of the IGST Act)

- Input Service Distributor (they have to file GSTR 6)

- Non-Resident Taxable person (they have to file GSTR 5)

- Composition Scheme Taxpayer under section 10. (they have to file GSTR 4)

- Tax Deductor at source under Section 51 (they have to file GSTR 7)

- Tax collector at Source under Section 52 (they have to file GSTR 8)

What is the penalty for not filing GSTR 1 Return?

A default notice under section 46 of the CGST Act will be served, in case any fails to file the return and will be liable to pay the tax amount along with interest on the outstanding amount. Per day penalty of Rs.100 will be applicable for each day of default up to a maximum amount of Rs.5000.

Effects on other Filings

GSTR 1 is the base document on the basis of which the rest of the returns are auto-populated. As the supplier of goods or services enters details of invoices raised by him towards the buyer of goods or services, an intimation of the same is sent to the buyer confirming the same in the form of GSTR 2A. Once the said transaction is confirmed at the buyer’s end, the details of which get auto-populated in the GSTR 2 at the suppliers end.

Or else, in case of discrepancy, this detail gets filed under GSTR 1A at the supplier’s end for further modification or rectification.

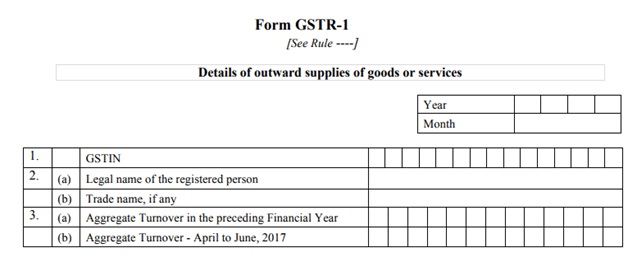

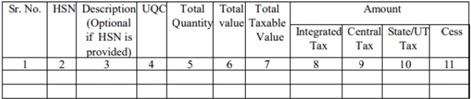

Particulars to be filed under GSTR 1

- GSTIN/Legal Name of the Entity/Aggregate Turnover for Previous Financial Year

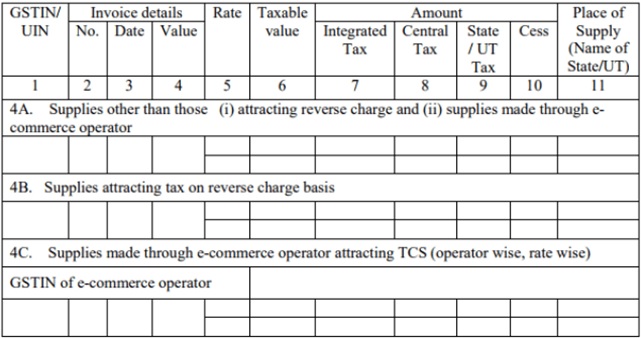

- Taxable Outward Supplies to Registered Persons

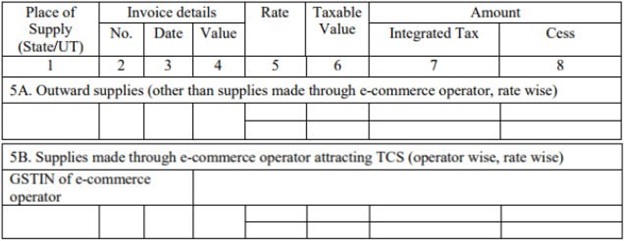

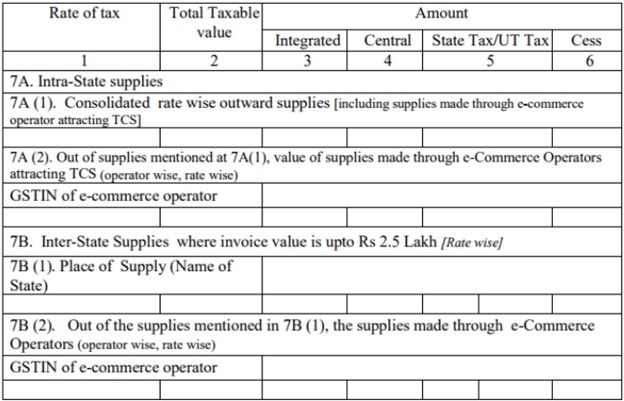

- Taxable outward inter-State supplies to unregistered persons where the invoice value is more than Rs 2.5 lakh

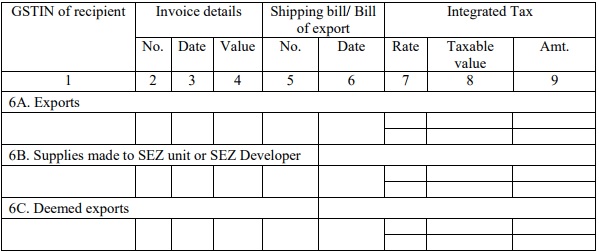

- Zero-rated supplies and deemed exports

- Taxable Supplies Made to Unregistered Persons

- Nil-rated, exempt and non-GST outward supplies

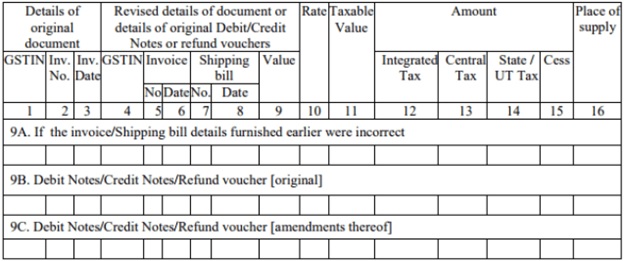

- Amendments to Taxable Supplies

- Amendments to taxable outward supplies to unregistered persons furnished on returns for earlier tax periods

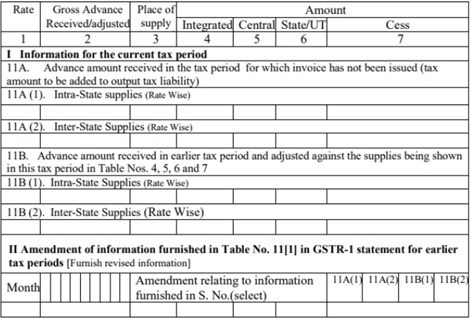

- Consolidated Statement of Advances Received or adjusted in the current tax period

- HSN-wise summary of outward supplies

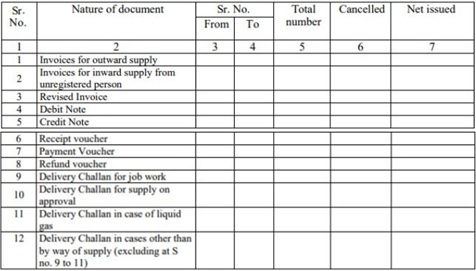

- Documents issued during the tax period