![The RBI [Reserve Bank of India]](https://ssrana.in/wp-content/uploads/2022/11/RBI-4-e1584959781469-1.webp)

RBI issues circular Limiting Liability of Customers in Unauthorized Electronic Banking Transactions

The Ministry of Corporate Affairs has notified the Companies (Incorporation) Second Amendment Rules, 2017 to amend the Companies (Incorporation) Rules, 2014, vide notification dated July 27, 2014.

The Ministry of Corporate Affairs has notified the Companies (Incorporation) Second Amendment Rules, 2017 to amend the Companies (Incorporation) Rules, 2014, vide notification dated July 27, 2014.

Applicability of GST on Lawyers and Law Firms

The Institute of Company Secretaries of India has announced that the Secretarial Standards on Meetings of the Board of Directors (SS-1) and General Meetings (SS-2) have been revised and the revised Secretarial Standards have received approval from the Central Government.

The Institute of Company Secretaries of India has announced that the Secretarial Standards on Meetings of the Board of Directors (SS-1) and General Meetings (SS-2) have been revised and the revised Secretarial Standards have received approval from the Central Government.

India: Mere failure of a corporate entity to meet contractual obligations is no ground for lifting of Corporate Veil

In Kirusa v. Mobilox, the National Company Law Appellate Tribunal passed an order interpreting the ambit of ‘dispute’ and ‘disputed debt’ for rejection of an application under Corporate Insolvency Resolution Proceeding.

In Kirusa v. Mobilox, the National Company Law Appellate Tribunal passed an order interpreting the ambit of ‘dispute’ and ‘disputed debt’ for rejection of an application under Corporate Insolvency Resolution Proceeding.

The Ambiguity surrounding Tobacco advertising in India

The Real Restate Regulation Act, 2016 requires real estate agents to register themselves. Section 2 (zm) defines a real estate agent who should register under the Act.

Cyber Cell Website launched by Delhi Police to ease filing of Complaints

As per recent news reports, a lot of confusion has been brewing as to whether any driver would be penalized for the passengers in his/her car being in an inebriated state. As per the initial news reports..

RBI issues circular Limiting Liability of Customers in Unauthorized Electronic Banking Transactions

Source: www.rbi.org.in

Rise of Digital Transactions

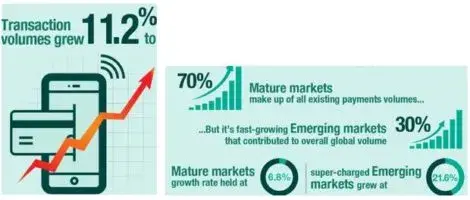

Commercial transactions, since the tail end of the last century, have been progressing towards the digital medium. Online retail, digital payments and availing of a plethora of services over the Internet was an inevitability, considering its rise and spread in the last 30-odd years. And non-traditional (i.e. cashless) payment methods have witnessed a meteoric rise over the last few years. According to the World Payments Report, 2017[1] , cashless transaction volumes grew 11.2% in 2014-2015 to reach a worldwide figure of 433.1 billion USD! This was fuelled largely by emerging Asian markets, including China, India and Hong Kong, contributing 43.4% of the global market transaction volume. Global payments volume was also driven by the emerging markets, which contributed 30% of the total, and grew at a whopping rate of 21.6% in the past year, as compared to only 6.8% growth of mature established markets.

Image Source: World Payments Report 2017

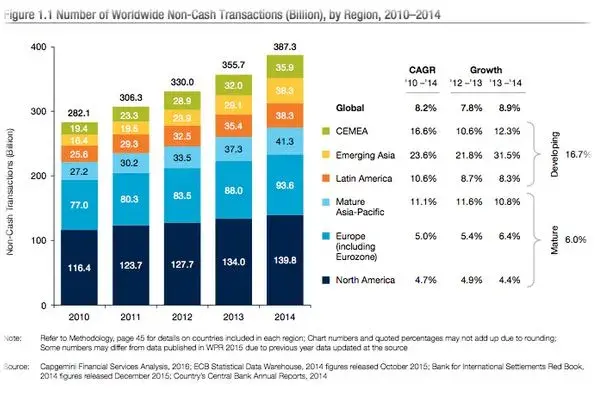

Image Source: Non-cash payments reach records, Banking Exchange, September 27, 2016

n electronic transaction is the sale or purchase of goods or services, conducted over computer-mediated networks; in which the goods and services are ordered over those networks, but the payment and the ultimate delivery of the good or service may be conducted on or off-line .[2]

However, along with the advent of digital transactions has come the curse of digital fraud. Customers newly introduced to cashless transactions and digital banking are often ignorant to basic precautions taken when transacting online, such as creating strong and secure passwords and PINs, not disclosing sensitive bank account information to third parties, avoiding accessing the Internet through public Wi-Fi networks, installing anti-virus and/or firewall protection, etc. Even banks and financial organizations are often seen to be woefully ill-equipped, in terms of having a secure data encryption system in place, adequate firewall protection, or secure storage of sensitive customer data. As a result, many people have fallen prey to hacking and digital fraud, with their accounts being compromised leading to significant losses. Credit card theft is also on the rise as petty criminals too become wise to the ways of profiting from cyber-crime.

The Government of India’s flagship project “Digital India”, envisions bringing government and public services, including the banking sector online, as far as possible, to increase convenience and accessibility to basic financial management for the majority of the population. Towards this, they have launched a number of schemes, such as Bharat Interface for Money (popularly known as BHIM), Unified Payments Interface (popularly known as the ‘UPI’), Aadhar Enabled Payment System (popularly known as AEPS), etc.[3] However, as has been seen with the recent massive hack of sensitive information of a number of banks[4] , customer confidence in online banking and digital transactions remains low.

To assuage customer uncertainty as well as to provide relevant useful operating guidelines to banks, the Reserve Bank of India (hereinafter referred to as ‘RBI’) has issued Circular DBR.No.Leg.BC.78/09.07.005/2017-18[5] on the subject of Customer Protection- Limiting Liability of Customers in Unauthorised Electronic Banking Transactions. This circular has revised the directions given to banks regarding the extent of customer liability in the case of unauthorized and/or fraudulent transactions given vide earlier Circular DBOD.Leg.BC.86/09.07.007/2001-02 dated April 8, 2002[6] , and it’s directives also supersede certain instructions contained in the RBI’s Master Circular DBR.No.FSD.BC.18/24.01.009/2015-16 dated July 1, 2015[7] , in light of the increased thrust on financial inclusion and customer protection measures, and the recent surge in customer grievances relating to unauthorized transactions conducted via their accounts or cards.

RBI Circular DBR.No.Leg.BC.78/09.07.005/2017-18: A Brief Overview

Objectives and Infrastructural Directives

The objective behind issuing revised directions regarding customer liability in cases of unauthorized transactions is that the systems and procedures in banks must be designed to make customers feel safe and increase their confidence in carrying out electronic banking transactions. The broad guidelines to ensure this are that banks must put in place:

- Appropriate systems and procedures ensure the safety and security of electronic banking transactions

- A robust and dynamic fraud detection and prevention mechanism

- A mechanism to assess the risks of unauthorized transactions and measure the liabilities arising therefrom

- Appropriate measures to mitigate such risks, and

- A system of continually and repeatedly advising customers on how to protect themselves from electronic banking and payments related fraud.

Banks are also directed to have their customers mandatorily register their mobile numbers for SMS alerts and, optionally, for email alerts regarding transactions made via their accounts or cards. Banks must also advise customers to report unauthorized transactions and stolen credit, debit or cash cards at the earliest, and informed that the longer they take to notify the bank, the greater the risk of loss/liability to the customer or bank. In order to assist customers to report loss or unauthorized transactions, banks must implement easily accessible and immediately responsive 24×7 notification systems, such as via website, SMS, phone banking, email, reporting to a home branch and a dedicated toll-free helpline. The time and date of every such notification must be recorded for the purpose of determining future liability (if any). The circular’s direction also states that a bank is not obligated to provide any further facility than ATM cash withdrawals to any customer who does not provide her/his mobile number.

Limited Liability of the Customer

The circular lays down that the customer shall be entitled to zero liability in cases of:

- Contributory fraud/negligence/deficiency of the bank

- Third party breach, where the deficiency lies neither with the bank, nor with the customer, but lies elsewhere in the system, and the customer notifies the bank within 3 working daysof receiving the communication from the bank regarding the unauthorized transaction.

The circular further lays down that the customer shall be limitedly liable in cases of:

- The customer’s own negligence or contributory action, such as in a case where the customer has herself/himself shared payment credentials. In such a situation, the customer will bear the entire loss until s/he has reported the unauthorized transaction to the bank. Any loss occurring after the reporting, shall be borne by the bank.

- Where the responsibility for the unauthorized e-banking transaction lies neither with the customer nor with the bank, but lies elsewhere in the system,

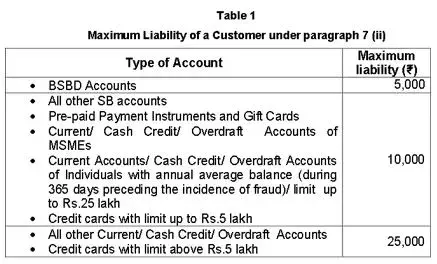

and where there is a delay of 4-7 working days after receiving the communication from the bank regarding the unauthorized transaction on the part of the customer in notifying the bank of such a transaction. In such a situation, the liability of the customer shall be limited to the transaction value, or the amount specified in Table 1 of the circular (reproduced below), whichever is lower.

- If the delay in reporting an unauthorized transaction, after receiving the communication from the bank regarding the unauthorized transaction, on the part of the customer exceeds 7 working days, the customer’s liability shall be determined as per the bank’s Board approved policy. The bank’s Board approved policy must be easily and publicly accessible, and must be supplied to each individual customer at the time of opening of their accounts. The customers must be kept updated about any changes to such policy.

Timelines for Redressal

The RBI circular stipulates exact timelines within which the customer should expect her/his problem to be redressed and/or compensation to be made. These are as below:

- 10 working days – On being notified by the customer, the bank shall credit the amount involved in the unauthorized transaction to the customer’s account within 10 working days from the date of such notification, without waiting for the settlement of insurance claim (if any). Banks are entitled to waive off any customer liability in cases of unauthorized electronic banking transactions, even in cases of customer’s own negligence.

- >

90 days – A complaint of unauthorized transaction must be resolved and any liability of the customer must be established within such time as stipulated by the bank’s Board approved policy, but which in any case may not exceed 90 days from the date of receipt of the complaint, and the customer must be adequately compensated. Where the bank is unable to resolve the complaint, or determine the customer’s liability (if any) within 90 days, then the compensation as outlined in the circular is to be paid to the customer.

Other Stipulations

The RBI circular also lays down that all banks must clearly define the rights and obligations of customers in cases of unauthorized transaction in specified scenarios and formulate/revise their customer relations policy with the approval of their respective Boards, and the directions laid down under the instant circular must be incorporated into any such policy. Such policy must be transparent, non-discriminatory, and lay down the methods and timelines under which the customers can expect to be compensated, and such policy must be prominently displayed, both in the bank’s physical premises as well as on their website, detailing its grievance handling and escalation procedures.

The burden of proving customer liability in all cases of unauthorized transactions shall lie on the bank.

The banks shall put in place a suitable mechanism and structure for the reporting of all customer liability cases to their Boards or to one of their committees, and all such transactions shall be reviewed by the bank’s internal auditors.

Conclusion

After the sudden note-ban exercise carried out by the Government on November 8, 2016, where 86% of India’s circulated currency in the form of 500 and 1000 rupee notes became de-valued overnight, there was a 400-1000% rise in digital transactions carried out across the country as citizens suddenly found that their physical money had been rendered useless! The move was one in which most Indians finally came to terms with alternative modes of payment, such as using their cards online, netbanking and mobile wallets. With cash having lost its pedestal, and the newer generations preferring digital forms of cash-free transactions, the RBI’s oversight on the risks inherent in the sphere of digital transactions is much needed, to maintain the customer’s confidence and provide her/him a peace of mind.

Additional References:

The Consumer Protection Act, 1986

RBI Bulletins 2016, 2017 at https://www.rbi.org.in/Scripts/BS_ViewBulletin.aspx http://digitalindia.gov.in/

https://www.worldpaymentsreport.com/

http://www.business-standard.com/article/technology/cashless-economy-india-

to-see-65-rise-in-mobile-frauds-in-2017-116121200523_1.html http://www.livemint.com/Money/KDDWmA7mjk3RnwY72hQ7nL/Going-digital-is-good-but-beware-of-risks.html http://economictimes.indiatimes.com/news/politics-and-nation/digital-frauds-on-a-rise-as-govt-harps-on-cashless-country/articleshow/56059761.cms

Applicability of GST on Lawyers and Law Firms

Source: www.livemint.com

The Delhi High Court vide its Order dated July 12, 2017, in the matter of J. K. Mittal & Company v. Union of India & Ors[1], has sought clarification from the Central Government and State Governments on whether all legal services provided by individual lawyers and law firms shall be governed by the “reverse charge” mechanism under the recently implemented Goods and Services Tax (hereinafter referred to as the ‘GST’) regime.

The issue was brought to the attention of the Delhi High Court by way of a writ petition filed by a proprietary concern of Mr. J. K. Mittal, Advocate who appeared in person before the bench and claimed that contrary to the recommendation of the GST Council at its 14th and 16th Meeting held on May 19, 2017 and June 11, 2017 respectively, the Centre and State Government issued Notification No. 13/2017 – Central Tax (Rate) dated June 28, 2017 and Notification No. 13/2017 – State Tax (Rate) dated June 30, 2017, which are per se in violation of CGST Act and DGST Act read with Article 279A of the Constitution of India.

According to the provisions of Article 279A, the various rates and slabs for GST under the CGST Act would be made only on the basis of the recommendations of the GST Council. While the recommendations of the GST Council were that for all services rendered by a lawyer or law firm, the service recipient would pay GST as per the “reverse charge” model, the Notifications issued by the Centre Government and Delhi Government prescribed that lawyers and law firms shall be liable to pay GST on all services rendered by them, except representational services where the recipient of the service, i.e., the client shall be liable pay GST.

The Bench comprising Justice S. Muralidhar and Justice Pratibha M. Singh observed that

“In view of the above submissions it is plain that as of date there is no clarity on whether all legal services (not restricted to representational services) provided by legal practitioners and firms would be governed by the reverse charge mechanism…In the circumstances, the Court directs that no coercive action be taken against any lawyer or law firms for non-compliance with any legal requirement under the CGST Act, the IGST Act or the DGST Act till a clarification is issued by the Central Government and the GNCTD and till further orders in that regard by this Court.”

The Court had directed the Centre and the State to provide sufficient clarification in this regard by the next date of hearing, i.e. July 18, 2017. In this subsequent session, various questions were raised as regards to a press release, presented by Mr. Narula, issued by the Press Information Bureau, Ministry of Finance, Government of India, on the position regarding applicability of GST on Legal Services provided by individual as well as a firm of Advocates. The legal sanctity of such a press release was questioned. It was also questioned whether the recommendations of the GST Council could be modified by virtue of a notification.

Mr. Narula then pleaded for more time on the issue that whether a lawyer or law firm who got registered under the Finance Act, 1994 could opt to de-register or surrender the registration. The Court ordered each of the Respondents to file a para wise reply to the petition and also specifically answer the queries as noted in the Court’s order dated July 12, 2017.

The Hon’ble bench further held that until any further orders, no coercive action would be taken against providers of legal services for non-compliance under the new indirect tax regime. The Court also held that all legal services provided by advocates, law firms, or LLPs of advocates will continue to be governed by the reverse charge mechanism unless any such legal service provider wanted to take advantage of input tax credit and opted for voluntary registration under Section 25 (3) of the CGST Act.

The case is now listed for hearing on14th September, 2017.

[1]W.P.(C) 5709/2017 & CM No. 23814/2017 (stay)

India: Mere failure of a corporate entity to meet contractual obligations is no ground for lifting of Corporate Veil

Source :www.linkedin.com

Facts

In a recent judgment delivered by the Delhi High Court in the case of Sudhir Gopi vs Indira Gandhi National Open University Indira Gandhi National Open University (hereinafter referred to as ‘IGNOU’ or ‘the Respondents’) and Universal Empire Institute of Technology (hereinafter referred to as the ‘UEIT’) entered into an agreement dated November 16, 2005, whereby UEIT agreed to act as a Partner Institute of IGNOU for three years. Mr. Sudhir Gopi (hereinafter referred to as the ‘Petitioner’), Chairman and Managing Director, UEIT, was designated to handle all further business between the parties on behalf of UEIT and not in his personal capacity. In the said agreement, both the parties agreed to share the fees collected from the students enrolled. The concerned parties entered into another agreement dated May 01, 2009, renewing the previous agreement for a further period. Consequently, disputes arose between the parties in connection with the agreement.

IGNOU pleaded that the invoices that were raised for admission and re admissions of students after July 2008 remained outstanding and only certain ad hoc payments were made. On the other hand, UEIT claimed that IGNOU had enrolled students from other institutes that were operating illegally outside the free trade zones, which resulted in higher expenditure to run a Centre in such zones. As a result, IGNOU terminated the agreement.

After invoking the Arbitration clause, IGNOU filed its claims followed by counter claims from Mr. Gopi and UEIT. In the arbitral proceedings, it was disclosed that Mr. Gopi, Chairman and Managing Director of UEIT and Mr. Nader Mohammed Abdulla Fikri were the only designated shareholders of UEIT. It was clarified that the reply to the statement of claims and the counter claim was filed by Mr. Gopi on behalf of UEIT in his capacity as the Managing Director and not in his personal capacity.

The Arbitral tribunal awarded a sum of USD 664,070 in favor of IGNOU against Mr. Gopi and UEIT, jointly and severally, along with interest at the rate of 12% p.a. on the awarded amount from January 03, 2012 to the date of the award.

Issue

- Whether there existed any arbitration agreement between Mr. Sudhir Gopi and IGNOU?

- Whether the decision of the arbitral tribunal to lift the corporate veil is sustainable?

- Whether this case falls within the scope of any of the exceptions to the rule for lifting of corporate veil?

Contentions of the Petitioner

The Petitioner claimed that the award by the arbitral tribunal was without jurisdiction as Mr. Gopi was also made liable for the awarded amounts. Relying on various judgments, the learned Counsel appearing for the Petitioner contended that an arbitral tribunal does not have the power to proceed against any person who was not a signatory to the arbitration agreement

Contentions of the Respondent

The Learned Counsel for the Respondents Mr. Aly Mirza contended that the Petitioner held 99 shares out of the 100 shares issued by UEIT and was the sole in-charge of running its affairs. He contended that it was plainly evident from the conduct of the Petitioner that he had made no distinction between himself and UEIT. He contended that the Petitioner was running the business under the façade of UEIT and essentially there was no difference between Mr. Sudhir Gopi and UEIT.

He further contended that prior to the commencement of the arbitral proceedings, IGNOU had issued a notice to UEIT and Mr. Sudhir Gopi, which was responded to by Mr. Gopi without registering any objection as to the notice being addressed to him directly. Similarly, Mr Gopi and UEIT had filed a common reply to the statement of claims and had also jointly filed counter claims

Court’s View

The Court stated that in the present case, neither the Agreement was signed by the Petitioner in his personal capacity, nor any of the communications produced provided a record of an agreement between the Petitioner and the Respondent to arbitrate. To add weightage to this view, the Court stated that both UEIT and Mr Gopi had clarified that Mr Gopi had preferred the counter claims on behalf of UEIT and not in his personal capacity vide the directions of the arbitral tribunal issued on April 30, 2015.

The Court categorically put forward its view that the arbitral tribunal, being a creature of limited jurisdiction, had no power to extend the scope of the arbitral proceedings to include persons who had not consented to arbitrate.

Relying on the judicial precedents put forth by the Petitioner, the Court stated that it is the Court who determines the question whether an individual or an entity can be compelled to arbitrate. In the case of Oil and Natural Gas Corporation Ltd. v. Jindal Drilling and Industries Limited, the Court held that the arbitral tribunal has no power to lift the corporate veil. Only a Court can lift the corporate veil of a company if the strongest case is made out. The Court inMV Tongli Yantai held that the mere fact that a party is an alter ego of another would not predicate an agreement to refer disputes to arbitration by the one which is not a party to the arbitration agreement. Courts have lifted the corporate veil to confer benefit or to foist liability upon a party.

Relying on an additional precedent in Indowind Energy Ltd. V. Wescare (India) Ltd the Court inferred that it is fundamental that a provision for arbitration to constitute an arbitration agreement for the purpose of Section 7 of the Arbitration and Conciliation Act, 1996, should satisfy two conditions: (i) it should be between the parties to the dispute; and (ii) it should relate to or be applicable to the dispute.

The Court further stated that all the judicial precedents relied upon by the Respondent have no application to the facts of the present case as either the subject matter in question was totally different (no dispute as to the existence of the arbitration agreement) or there was no quarrel with the proposition that the corporate veil could be lifted

The Court stated that arbitration is founded on consent between the parties to refer the disputes to arbitration. The fact that an individual or a few individuals hold controlling interest in a company and are in-charge of running its business does not render them personally bound.

The Court answering the query in relation to extending an arbitration agreement to non-signatories, held that it can be done in limited circumstances, first, where the Court came to the conclusion that there was an implied consent and second, where there were reasons to disregard the corporate personality of a party. It further stated that a corporate veil could be pierced only in rare cases where the Court came to the conclusion that the conduct of the shareholder was abusive and that the corporate façade was used for an improper purpose.

Judgment

The Court held that there was no foundation that the corporate façade of UEIT had been used by Mr. Sudhir Gopi to perpetuate a fraud. Mere failure of a corporate entity to meet its contractual obligations was no ground for piercing the corporate veil. The Court further stated that the alter ego doctrine was essentially to prevent shareholders from misusing corporate laws by a device of a sham corporate entity for committing fraud. The Court also held that in accordance with the facts of the case, there was no ground to disregard the corporate form of UEIT.

The petition was allowed and the impugned award as regards to the Petitioner was set aside.

[1]O.M.P (COMM) 22/2016

[2]Balmer Lawrie & Company Ltd v. Saraswathi Chemicals Proprietors Saraswathhi Leather Chemicals (P) Ltd, EA(OS) No. 340/2013, Great Pacific Naviigation(Holdings) Corporation Ltd v. M V Tongli Yantai 2011 LawSuit(bom) 2095, Prakash Industries Ltd. v. Space Capital Services Ltd.: 2016 SCC OnLine Del 6140, Oil and Natural Gas Corporation Ltd. v. Jindal Drilling and Industries Limited: 2015 SCC OnLine Bom 1707

[3]Union of India (UOI) v. M/s. Pam Development Pvt. Ltd.: (2014) 1 SCR 1069, Purple Medical Solutions Pvt. Ltd. v. MIV Therapeutics Inc. and Ors.: 2015 (2) SCALE 127, Ram Kishan and Sons v. Freeway Marketing (India) (P) Ltd. and Anr.: 2004 (2) ArbLR 508 (Delhi)

The Ambiguity surrounding Tobacco advertising in India

On May 21, 2003, the World Health Organization Framework Convention on Tobacco Control (hereinafter referred to as the ‘FCTC Treaty’) was adopted by the 56th World Health Assembly. The said treaty was one of the most quickly ratified treaties in the United Nations history, and it seeks to, “protect present and future generations from the devastating health, social, environmental and economic consequences of tobacco consumption and exposure to tobacco smoke”. It seeks to achieve this objective by enacting a set of universal standards stating the dangers of tobacco and limiting its use in all forms worldwide. It has been signed by 168 countries and is legally binding in 180 ratifying countries. There are however, 16 United Nations member states that are non-parties to the treaty. Thus, one can say that there is a certain sense of worldwide uniformity related to promotion and advertising of tobacco related products.

However, in India, advertising related to tobacco products is following a different trend, as the industry has now shifted focus to advertising at point of sale outlets i.e., a place in the wholesale or retail environment where tobacco products are sold, like retail shops and tobacco kiosks. As reported on July 19, 2017, by a leading Indian news daily LiveMint, many tobacco products are still being advertised on the boards of shops which are being prepared and erected by the company manufacturing or distributing the concerned product.

Similarly, the display of products or advertisements inside many shops is also done on a regular basis. In its attempt to sell as many tobacco products as possible, the tobacco industry uses a great variety of direct and indirect approaches with the aim of promoting its use. Point of sale tobacco advertisements have been observed not only on shops selling tobacco products, but also on shops generally not selling tobacco products. The said news article also stated that most of these tobacco kiosk owners receive payments in the form of monthly fees and even receive free cigarettes as an incentive to put hoardings that promote these tobacco products. Thus, hoardings are being placed outside establishments that may or may not be selling tobacco products with huge, colorful backgrounds mimicking the colors and design of different brands of tobacco, including pictures, descriptors, backlighting, and other eye-catching decorative embellishments

The fact that exposure to promotional activities for tobacco leads to initiation of tobacco use, is not unknown. Such exposure to tobacco advertisements and receptivity to tobacco marketing in turn has led to increasing tobacco use among students, an age category that has now become a target audience for cigarette and tobacco companies. Given its immense population, India has always been a high potential market as the target audience for the cigarette market falls within the age group of 18-24 Years.

The Government of India, to combat this issue, came up with the Cigarettes and Other Tobacco Products (Prohibition of Advertisement and Regulation of Trade and Commerce, Production, Supply and Distribution) Act in 2003 (hereinafter referred to as ‘the Act’) and subsequently also signed FCTC Treaty, placing a comprehensive ban on tobacco advertising, promotion and sponsorship (TAPS). The Act sets out a number of stringent regulations to address tobacco promotion, with the exception of point of sale and on-pack advertising. Section 5 (1) of the Act states that “No person engaged in, or purported to be engaged in the production, supply or distribution of cigarettes or any other tobacco products shall advertise and no person having control over a medium shall cause to be advertised cigarettes or any other tobacco products through that medium and no person shall take part in any advertisement which directly or indirectly suggests or promotes the use or consumption of cigarettes or any other tobacco products.” A plain reading of the above section suggests that there is complete prohibition on all direct and indirect advertisements of tobacco products. The said prohibition is in consonance with Article 13 of the FCTC Treaty and also extends to any activity that promotes the use or consumption of cigarettes or any other tobacco products. Thus, Section 5 of the Act prohibits any kind of advertisement, be it direct or indirect. The Ministry of Health and Family Welfare clarified the definition of an ‘indirect advertisement’, vide its notification GSR 345(E), dated May 31, 2005. It stated that ‘indirect advertisement’ means (a) the use of a name or brand of tobacco products for marketing, promoting or advertising other goods, services and events; (b) the marketing of tobacco products with the aid of a brand name or trademark which is known as, or in use as, a name or brand for other goods and service; (c) the use of particular colors and layout and/or presentation that are associated with the particular tobacco products; and the use of tobacco products and smoking situations when advertising other goods and services.

Though, the Act places a complete ban on any sort of advertisement of tobacco products, but the rules to the Act provide for a partial allowance with regard to it. Sub Clause 1 to Rule 4 of Cigarettes and Other Products (Prohibition of Advertisement and Regulation of Trade and Commerce, Production, Supply and Distribution) Rules, 2004, states that “the size of the board used for the advertisement of cigarettes and any other tobacco products displayed at the entrance of a warehouse or a shop where cigarettes or any other tobacco products is offered for sale shall not exceed sixty centimeters by forty-five centimeters.” Thus, it allows advertising of tobacco products but with certain limitations. According to the above-stated rule, tobacco products can be advertised in the package containing such products and also at the entrance and inside a warehouse storing tobacco products with a limitation that such public advertising can address only the type of tobacco products, and products that have no brand pack photo, brand name or other promotional message and picture. The Rules further state that the display board shall not be backlit or illuminated in any manner. Rule 4 (2) provides the guidelines for retail shops to display ‘Tobacco causes cancer’, or ‘Tobacco kills’ at the top edge of the board in a prominent manner measuring twenty centimeters by fifteen centimeters. Hence, retail shops that display cigarette packets with their brand names are at fault and can be held liable under the provisions of the Act. A major violation of the Act relates to the size of the board of advertisement. In most cases, the size of the board is equal to the frontal width of the shop, with each advertisement equaling the prescribed size and rest of the board being blank or bearing a picture.

This enhanced impression surely attracts youngsters, who find pride in smoking cigarettes. Advertisements on cigarette packets or on billboards and hoarding outside retail shops, works manifold in pulling the college crowd towards the apparent negatives of tobacco use. The Allahabad High Court, in its celebrated judgment in the case of Love Care Foundation v. Union of India and Anr., stated that plain packaging is associated with lower smoking appeal and more urgency to quit among adult smokers. The Court relied on the fact that plain packaging of cigarettes has had positive outcomes in Australia, Brazil and Ireland, wherein, branded packets were considered more appealing and better tasting. Thus, such packaging was banned, which resulted in substantial decrease in the quantity of cigarettes people smoked. The Court reached to a conclusion that plain packaging and removal of descriptions may reduce the appeal of smoking for youth and young adults, and consequently reduce smoking susceptibility. The Court stated that Tobacco plain packaging measure would be a long term investment to safeguard the health of the Indian youth. The Hon’ble Allahabad High Court, keeping in view the above contentions, advised for promotion of plain packaging, wherein, the name shall be displayed only on a restricted part of the packet, while the rest of the packet will portray health warnings as required under the Rules of 2005.

Such a ruling by the Hon’ble Court in favor of plain packaging of tobacco products is a welcome change and a step forward in improving the health of citizens. After carefully studying the effect and trend in various other countries like Australia and Brazil, it can be confidently concluded that plain packaging would lead to a positive change. Putting restrictions on retail shop owners to not advertise cigarette and other tobacco products based on their brand names, coupled with plain packaging can work towards reducing the sales of cigarettes in the country.

Such a ruling by the Hon’ble Court in favor of plain packaging of tobacco products is a welcome change and a step forward in improving the health of citizens. After carefully studying the effect and trend in various other countries like Australia and Brazil, it can be confidently concluded that plain packaging would lead to a positive change. Putting restrictions on retail shop owners to not advertise cigarette and other tobacco products based on their brand names, coupled with plain packaging can work towards reducing the sales of cigarettes in the country.

See ‘Cigarette companies woo young people in India while health officials are fuming’, LiveMint, Wednesday July 19, 2017

Writ Petition No.1078 (M/B) OF 2013

Cyber Cell Website launched by Delhi Police to ease filing of Complaints

Source: www.delhipolice.nic.in

The Cyber Crime Cell of the Economic Offences Wing, Delhi Police officially launched its website www.cybercelldelhi.in on July 26, 2017 to facilitate online filing of complaints in matters concerning online scams and security. The system has been christened ‘Delhi Police Online Complaint Lodging System for Economic and Cyber Offences’.

Citizens can now file online complaints against cyber offences without having to go to the Police Station physically. The system requires a user registration which can be easily obtained by providing e-mail address and phone number. The website also provides pre-emptively, a list of documents required for filing a complaint relating to various types of cyber offences.

This comes as an addition to the already present facilities with the Cyber Cell like the cyber lab for investigating cyber forensics. The website contains information about different types of offences committed online namely, Email Frauds, Social Media crimes, Mobile App related crimes, Business Email Compromise, Data Theft, Ransomware, Net Banking/ATM Frauds, Fake Calls Frauds, Insurance Frauds, Lottery Scam, Bitcoin, Cheating Scams, and Online Transactions Frauds. Further, the website also provides helpful guides for citizens to stay vigilant online with different sets of tips for Cyber Safety addressed to Children, Women, Parents, Senior Citizens, Business-persons and Internet Banking users.

Mr. Amulya Patnaik, Commissioner of Delhi Police, has stated that women and young school-going children are easy targets and are even more vulnerable to cyber-crimes due inadequate awareness of online threats and safe online habits. Therefore, as part of its initiative, the Cyber Crime Cell has been organizing campaigns among the school children and teachers from time to time.

As assured by the Commissioner Mr. Patnaik, we trust that the Cyber Crime Cell would make all efforts for expeditious and effective prosecution and disposal of these complaints.

Source: www.cybercelldelhi.in